Download the Transportation SOTM Here

Another year of planning for the unplanned. The onset of the COVID-19 pandemic in 2020 ushered in an era of unpredictability that has persisted well into 2023. A black swan event, the pandemic upended many aspects of the world we live in, forcing the transportation industry to adapt to a never-ending slew of challenges.

The cost of owning and operating a fleet only seems to grow with every passing year, and this includes the price of insurance. Though the current insurance market is one of the most challenging we have seen in years, it is still an essential investment for transportation companies that want to protect their business from unexpected monetary shocks.

Unfortunately, many of the same issues are negatively impacting both the transportation industry and the insurance carriers that support transportation companies. At times, these shared challenges have put both transportation operations and carriers in what seems like a head-on collision. As we detail below, these overlapping issues feed into each other.

Despite the significant headwinds, the transportation industry is an indispensable component of the economy. Because of the strong demand for transportation services, there are ample business opportunities for the industry, but fleet owners need to understand and be able to adapt to today’s risks and insurance market conditions. Fleet owners have the power to proactively minimize their financial exposures by investing in preventive measures, which are likely to reduce the probability of a loss, improve business performance, and result in optimal rates from carriers.

Owning and operating a fleet is a complex undertaking, and even more so in today’s environment. We understand that you have to balance wide-ranging, competing priorities, with insurance and risk management being just part of the puzzle. Just as the transportation industry is multifaceted, so too are the insurance products that support it. Because of this, you will want to work with an insurance advisor with proven expertise in not just the insurance industry, but also transportation. Our team of transportation insurance experts knows how to craft tailored risk management strategies and find insurance coverage solutions for transportation companies – from smaller operations to those that span borders, that carry all types of cargo – we know how to help you build a culture of risk management and safety that protects your bottom line.

Transportation – Key Industry Challenges

Well into 2023, an all too familiar set of exposures continues to challenge the transportation industry, and fleet owners need to be aware of the potential impact of these risks.

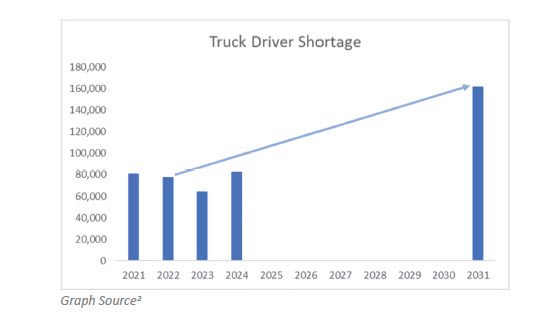

Driver Shortages: The transportation industry has been at the front lines of the supply chain issues of recent years, with worker shortages in the industry being one of the driving forces behind bottlenecks. The American Trucking Association (ATA) estimates the U.S. trucking sector was 78,000 drivers short in 2022¹. Based on current trends, the ATA also estimates that the driver shortage could top 160,000 drivers over the next decade. There are many factors behind the labor shortage in the trucking industry. These include perceptions of the transportation industry, demographic challenges, skill gaps, and a shifting mindset toward work.

For starters, Baby Boomers and Gen X are exiting the labor market for retirement, which is leaving a talent gap in the transportation industry. Because our culture traditionally devalues trade jobs, this makes it difficult for fleet owners to attract and retain new talent. And once a younger employee is hired, their skill level might not be on par with someone who has been on the job for decades. Another major issue impacting the transportation industry is that many workers do not have the necessary skills for job openings. With an uptick in demand for skilled labor, many training programs haven’t been able to keep up, leading to a shortage of qualified workers. Finally, workers also want jobs that provide a good work-life balance, which is something that transportation jobs have historically been unable to provide.

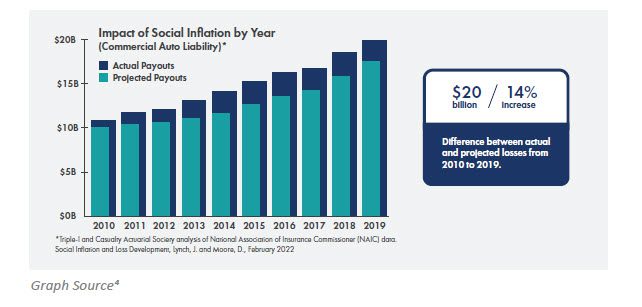

Nuclear Verdicts: Commercial fleets have been some of the top targets of litigation funded by third parties, which run the risk of resulting in hefty verdicts. The Insurance Information Institute estimates that social inflation increased claims by an estimated $20B (14%) from 2010 to 2019 in commercial auto liability³. Social inflation describes the rising cost of insurance claims as a result of increased litigation, plaintiff-friendly legal decisions, broader contract interpretation, and larger jury awards, and is the driving force behind nuclear verdicts. This is when a jury provides an award in a case that’s more than $10 million, an amount so high that it surpasses what most people would consider reasonable. As nuclear verdicts grow in size, so do commercial auto liability rates.

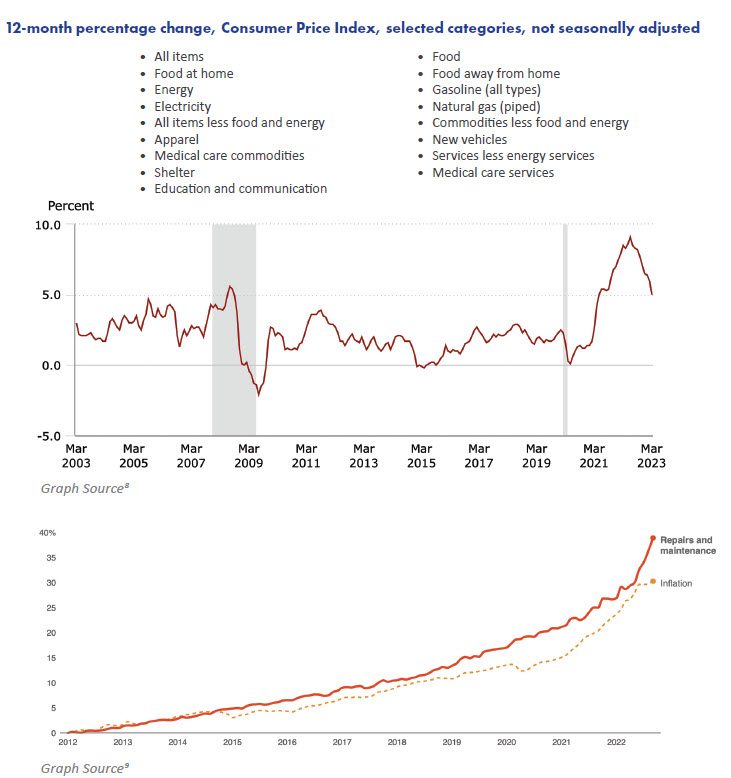

Economic Pressures: Economic uncertainty driven by higher interest rates, inflation, and decreased consumer demand will likely persist throughout 2023. Throughout 2022, inflation climbed to a peak of 9.1% in June⁵ and closed out at about 7% in December. As of February 2023, inflation seemed to be slowing, coming in at 6% for the 12-month period⁶. Inflation impacts fleet operations in a number of ways. It drives up operational costs and the pricing of raw materials for companies, greatly increasing repair costs for vehicles and the price of purchasing new autos for fleets. Higher production costs for new vehicles have prices up 4.2% year-over-year as of January 2023⁷.

Fuel Costs: The Russia-Ukraine war has had a far-reaching effect on the global economy by further straining global supply chains, pushing up inflation, and increasing global energy prices. With fuel costs being one of the highest line items on fleet budgets, rising prices dramatically impact transportation companies. In June of 2022, gas prices for all formulations reached an all-time high, averaging $5.03 in the United States¹⁰. Though prices have dropped to an average of $3.50 a gallon as of February 2023, fuel price volatility creates layers of unpredictability that challenge fleet owners’ ability to properly forecast and control costs.

Supply Chain Issues: Ongoing supply chain issues continue to hamper the transportation industry as constraints and interconnection bottlenecks have caused manufacturers to struggle to meet demand for vehicle components. This means that parts needed for vehicle repairs are harder to come by, and that there are delays in the production of new cars. Supply chain issues have forced fleets to keep utilizing assets beyond preferred timelines. This drives up maintenance costs and downtime, and can also negatively impact insurance rates. And when new assets or car components do become available, the demand for them makes acquiring them a competitive process, with fleet owners flocking to get whatever they are able to get their hands on.

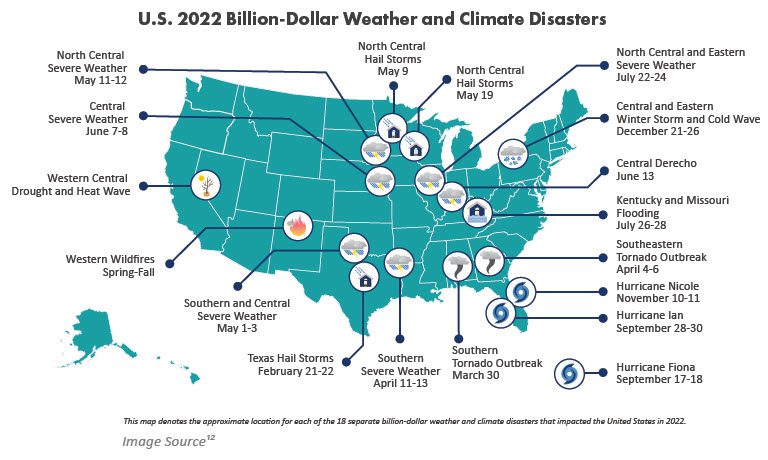

Natural Disasters: 2022 was yet another year plagued by extreme weather events, with 18 climate disaster events surpassing the $1 billion mark in damages in the United States alone, amounting to $165 billion in insured and uninsured losses¹¹. Extreme weather events impact the transportation industry’s ability to deliver freight safely and on time, often forcing operations to halt within impacted areas. Inclement weather also increases the likelihood of repairs, as the elements wear down tires, windshield wipers, car batteries, and more. Additionally, natural disasters can also worsen supply chain issues as manufacturing operations in the path of extreme weather events may be forced to close, while also impacting worker availability.

Cyber Threats: Cyber security continues to be a risk for the transportation industry in 2023. As transportation companies continue to increase their dependence on automation tools and advanced telematics, they need to be aware of how virtually connected systems bring forth monetary and reputational risks to critical business operations. To put things into perspective, the average cost of a data breach is expected to exceed $5 million in 2023¹³. A successful cyber attack that compromises in-cab systems also has the potential to shut down a vehicle and thus endanger the driver and others. Cyber exposures also expand beyond internal systems and include cyber risks from vendors in the supply chain. Additionally, geopolitical conflicts, like the war in Ukraine, increase the likelihood of cyber attacks, with state-sponsored malicious actors zeroing in on critical industries in their exploits.

Regulatory Environment: Transportation companies need to be attuned to compliance requirements at the local, state, and federal levels. For entities with international operations, cross-border compliance also comes into play. Adhering to the U.S. Department of Transportation’s (DOT) regulations means that fleet owners need to maintain records of driver inspection reports, hours of service logs, international fuel tax agreement reports, employee substance use test results, and more. Transportation companies also need to be sure that they comply with employment laws across state lines and carry the proper workers’ compensation coverage for the states in which they operate.

The transportation industry is also greatly affected by efforts to transition to a low-carbon economy. As more states pass legislation that requires fleets to transition to low-carbon emission models, fleet owners are being forced to change their operations accordingly, while having to meet current global demands for their services and growing operational costs. Navigating this complex web of regulations can be grueling, and failure to adhere to the rules can result in costly fines and legal fees.

Freight-Specific Risks: Transportation companies move all types of freight from one place to another – people, animals, liquids, hazardous materials, flammable items, food – the list goes on. And each type of conveyance is going to have its own set of challenges and associated risks, which fleet owners need to be aware of in order to manage them appropriately.

Primary Insurance – A Hardened Market

Fleet owners everywhere might have experienced sticker shock when it has been time to renew their insurance, with most lines of coverage seeing price increases in recent years. As transportation companies look to justify their insurance spend in the midst of so many challenges and overarching growing operational costs, understanding the driving forces behind these increases is the first step in managing the price of your insurance portfolio.

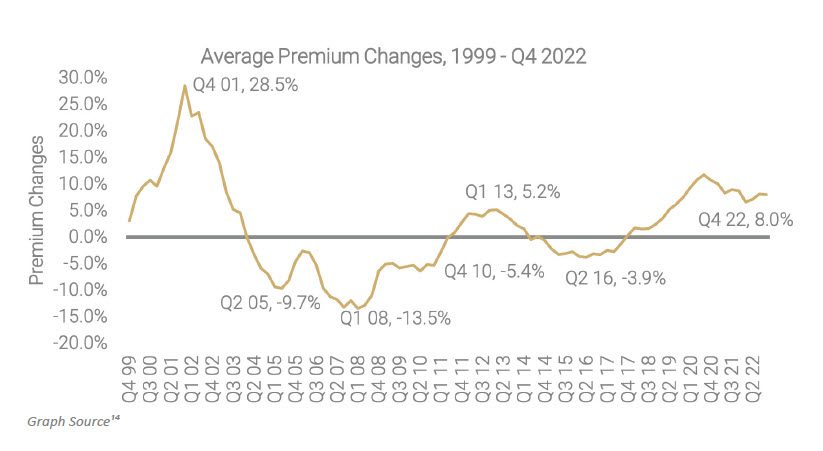

Primary Insurance Market Capacity: Just as insureds are having to grapple with growing operational costs and risks in the face of unpredictable global events, so too are insurance carriers. Continuous negative underwriting results have caused the property and casualty (P&C) market to harden, which means premiums are higher, carrier capacity is diminished, and underwriting scrutiny is heightened.

Why the P&C Market Has Hardened

Economic pressures, such as inflation and the threat of recession, make it difficult for carriers to maintain pricing and keep pace with unpredictable loss patterns. In a high inflationary environment, loss expenses increase, which can result in higher loss ratios for carriers. Furthermore, insurance carriers are as susceptible as all businesses to the threat of a recession, which economic experts fear is on the horizon due to rising interest rates, sustained labor challenges, and reduced economic activity.

Supply chain disruptions brought on by increased demand and slowed production during the COVID-19 pandemic continue and are exacerbated by labor shortages and geopolitical conflict. Supply chain issues have led to a shortage of raw materials. This creates manufacturing delays, drives up repair costs, and increases losses for carriers.

Persistent labor shortages caused by the Great Resignation and an aging workforce in key industries, including construction, manufacturing, and transportation, worsen supply chain issues. Labor shortages in the manufacturing industry mean that there are fewer available workers to meet labor demands in regions that experience severe losses due to extreme weather events. To attract and retain talent, employers are raising wages, which is another factor contributing to growing replacement costs. Carriers are struggling to adapt risk models to account for growing wages in key sectors.

Geopolitical unrest has had far-reaching consequences, particularly the Russia-Ukraine conflict. This war has further hampered an already strained supply chain. Additionally, international conflicts also heighten cyber security concerns for businesses, and threaten a cyber insurance market with limited capacity.

Extreme weather events are reshaping the world as we know it. The insurance industry has yet to adapt underwriting strategies and climate models to the nature of interconnected weather events. Recurring natural disasters amount to an increased severity in insurance claims, and when carriers experience year after year of high loss patterns, this could threaten their ability to remain solvent.

Social inflation has ushered in the era of nuclear verdicts, with carriers having to foot the bill for litigation and multimillion-dollar jury awards. When we consider verdicts that surpass the $1 million mark, from 2010 to 2018, the average size of verdicts increased almost 1,000 percent, rising from $2.3 million to $22.3 million¹⁶. And in 2022, the median verdict ballooned to $41.1 million while the number of verdicts also doubled¹⁷.

What Can Insured Expect from the Current Market?

Though the primary insurance market is feeling pressures from many directions and responding accordingly in a manner that transportations companies are having to navigate, the availability and terms of coverage for insureds will vary greatly by insurance line, loss history, and implementation of loss controls. Here is what buyers should expect from the current market:

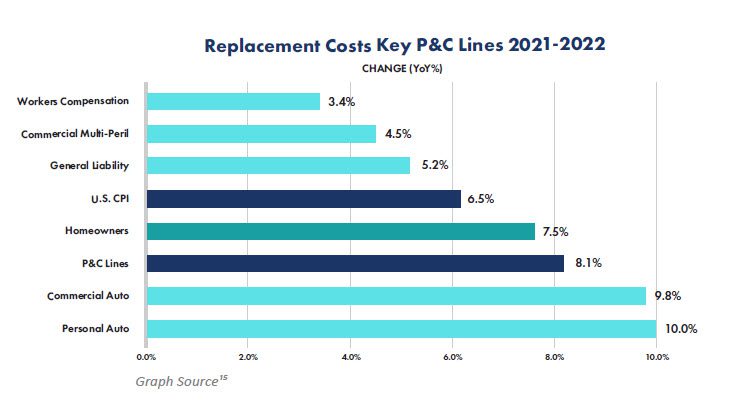

Intensified Focus on Valuations: Seesawing replacement costs, as a result of inflation, supply chain issues, and labor shortages, have made it challenging for carriers to properly price coverage, resulting in significant losses year over year. The combination of these factors paired with the trend of insureds undervaluing assets or failing to update the value of assets has made insurance carriers zero in on valuation of assets during the underwriting process. Carriers hope that this will help them improve modeling and price coverage more accurately so they can improve loss ratios. However, insurer replacement costs are projected to increase between 4.5% and 6.5% in 2023¹⁸.

Evidence of Loss Controls: With increased underwriting scrutiny, insureds need to take the necessary steps to implement loss controls within their business operations. Underwriters will want to see documentation that paints a clear picture of the risk they are taking on and will ask for evidence of both proactive and reactive loss controls that insureds have implemented. Proactive loss controls are the actions insureds take to mitigate future risks and prevent claims from happening, while reactive loss controls are the plan of action insureds take in the event of a loss to prevent similar events from happening again in the future.

Relationships with Carriers Matter: Building and investing in a relationship with carriers over the years pays dividends in a hardened insurance market. Clear and active communication with underwriters throughout the underwriting process is especially crucial for insureds with complex risk profiles, as meaningful conversations are more likely to result in favorable coverage terms. Companies that demonstrate they have invested in building a culture of risk management are likely to cultivate positive relationships with underwriters, which may also put insureds in a better position to negotiate policy terms.

Natural Catastrophes Limiting Capacity: 2022 global insured and uninsured losses amounted to about $270 billion, following $320 billion in total losses in 2021¹⁹. Year after year of high losses means that carriers are retreating from riskier markets, which can make it increasingly difficult for insureds to find nat cat coverage. And when coverage is available, insureds in disaster-prone areas may see exorbitant rate hikes, restrictive terms and conditions, higher retention levels, and an overall reduction in limits. Experts predict a 10% to 25% increase in commercial property insurance premiums in 2023, though this number could be higher for property in disaster-prone areas²⁰.

Though businesses in disaster-prone areas are seeing greater increases, price hikes are hitting most markets around the country, even those that don’t experience many natural disasters. This is because extreme weather events have been so bad for such a long time that they’re even beginning to impact the reinsurance market, which we explain in more detail below.

Commercial Auto Liability Rate Hikes: Commercial auto insurance continues to be a challenging market. Loss severity has risen substantially because the cost to repair damaged vehicles has escalated due to inflation, supply chain issues, and nuclear verdicts. Additionally, with newer vehicles being equipped with modern technology, like sensors, computer chips, and cameras, this also increases repair costs. Commercial auto rates rose 7% in Q4 of 2022²², though our team of transportation insurance advisors is seeing rate increases of up to 30% in 2023.

Workers’ Compensation Remains Stable: Amidst overarching turmoil, workers’ compensation remains stable and has ample capacity, with rates continuing to drop. In the U.S., average premium renewal rates declined 1.48% in Q4 2022 on top of a 1.08% decrease from the previous quarter.

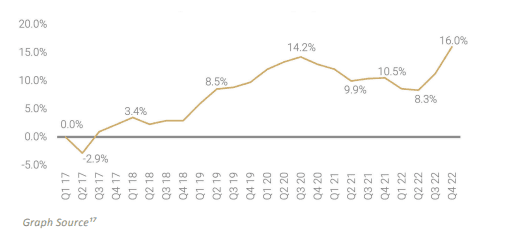

Excess Liability Pricing Pressures: Excess liability layers are experiencing pressure from social inflation, which has resulted in growing jury awards. Rate increases averaged 9.6% in Q4 2022²³, though riskier profiles will see higher pricing increases.

Reinsurance Market Capacity

Even the reinsurance market is feeling the impact of macro socioeconomic trends. While the primary insurance market covers financial liability for policyholders as a result of a triggering event, reinsurance is insurance for insurance companies that helps them remain profitable and in business. However, certain risks like natural disasters can be large enough to expose even the reinsurance market and reduce its capacity. Property lines have faced margin pressure because pricing has not kept up with sustained high inflation, the effects of climate change, and oscillating repair and construction costs.

Natural Catastrophes: Unrelenting claims from catastrophic natural disasters and the threat of climate change are severely impacting reinsurers’ position. Because reinsurers have a global footprint, natural catastrophes that occur around the world in addition to those we experience in the United States result in higher rates for primary insurers. This cost is then passed down to policyholders, such as fleet owners, even if their operations are not based in areas that experience extreme weather events.

Significant losses after catastrophic natural disasters have investors fleeing to other markets with higher potential returns. With extreme weather events showing no sign of slowing down and the threat of recession looming, these issues are likely to worsen.

Additionally, projections from catastrophe models have claim expenses increasing up to 30% because of growing cost and availability of materials and labor, among other factors. Due to the growing number and cost of losses across the U.S. and the number of poorly capitalized carriers in geographic areas that have seen continuous natural disasters, reinsurers are expected to bear the brunt of these extreme events.

Premium increases from reinsurers in 2023 are a result of inflation and record-breaking natural catastrophe losses. Reinsurance rate increases for property catastrophe business have averaged 37%, according to Howden’s index²⁵.

How the Transportation Industry Can Answer the Call

Though you might not be able to control the insurance market and all variables that are driving the cost of premiums upward, there are things that you can do to get optimal coverage results for your business’ exposures and risk tolerance. This includes investing in the right technology and loss controls. Taking these steps has a twofold benefit – you improve your fleet’s operational efficiency, and you demonstrate a culture of safety to carriers – both of which result in cost savings.

To successfully withstand significant pressures and a dynamic risk landscape, the transportation industry will need to take advantage of these key areas of opportunity.

Driver Recruitment & Retention

Though the shortage of drivers is a complex issue with no simple solution, there are steps that transportation companies can take to recruit drivers, including the following:

- Recruit a New Class of Drivers: Recruitment efforts should try to attract a new class of drivers by focusing on different demographics, including women and younger people. Transportation companies can also consider tapping into veteran transition programs.

- Reimagine Recruitment Efforts: Fleet owners have an opportunity to leverage social media and an online presence to attract younger workers. Consider partnering with high schools, local colleges, and trade schools to attract new workers, and also sponsoring students’ commercial driver’s license (CDL) training.

- Offer Competitive Wages: With the cost of living growing, drivers expect higher wages. Though it might be challenging to pay drivers more in the face of growing operational costs, consider the cost of turnover on your bottom line. If your company cannot afford higher-than-planned wage hikes at this time, you can leverage the power of your benefits program to let employees know what you are already doing to put more money in their pockets.

- Provide Holistic Benefits: Driver retention continues to challenge transportation companies, which is why offering comprehensive benefits is key to attracting and retaining drivers. To manage the cost of benefits, align your offerings with employees’ needs and wants by getting their feedback. You also have the option of exploring various plan design options that can result in cost savings.

- Make the Job More Manageable: Drivers want to work for companies that offer a strong culture that makes them feel valued. Consider providing mentorship programs, training programs based on experience, mental health support, and wellness programs.

Telematics

Harnessing the power of telematics is one of the best strategies businesses can use to control the risks and costs of owning and operating a commercial fleet. Telematic solutions are GPS and cameras that allow you to identify where a vehicle is and has been, what it is and has been doing, as well as the happenings around the vehicle. In addition to helping transportation companies manage their costs and stay on top of maintenance issues, telematics are a mandatory prerequisite for coverage for many insurers. These programs can help reduce fleet costs in a variety of ways, including:

- Identify Risky Behaviors: Risky driving increases the likelihood of preventable accidents. Telematics monitors actions, such as rapid acceleration, harsh braking, and frequent lane changes. This information allows you to take corrective action with your employees. Not only does this help prevent potential collisions, but it also boosts productivity, improves safety, and decreases wear and tear on vehicles, leading to potential savings. Don’t just correct risky behavior—prioritize rewarding your responsible drivers.

- Keep up with Maintenance Cycles: Certain telematics programs keep track of necessary vehicle maintenance so you can be proactive in your servicing before issues arise. Utilizing a system that monitors check engine lights, tire pressure, and other service alerts helps you remediate issues before they become more severe and costlier to fix.

- Manage Business Expenses: The use of telematics data can help you identify areas to cut costs. One of the biggest money pits in owning a fleet is the unnecessary idling of engines. Idle engines burn through gas and contribute to significant wear and tear over time. Tracking fuel efficiency through telematics can identify instances of engine idling, as well as ensure drivers take the best available route to optimize fuel usage.

- Claims Management and Mitigation: Telematics can provide valuable data that proves innocence from a liability standpoint and even highlights instances of fraud. For example, if someone cuts in front of your driver and slams on their brakes, telematics will show that your driver was not at fault or indicate the other driver’s actions were unsafe or even purposefully negligent.

- Underwriting Benefits: Underwriters like to see robust information, and telematics does a great job of providing exactly that. Taking a proactive approach to risk mitigation makes you more appealing as an insured. Proving that your business is using telematics as a coaching tool to correct risky driving behavior shows your commitment to road safety and can help lower your rates. In addition, the more data carriers have about your operation, the more accurate the pricing.

When using telematics, be sure to communicate with employees and address any cybersecurity vulnerabilities to prevent a data breach.

Route Optimization

In light of a driver shortage and growing fuel costs, fleet owners should make use of route optimization software that can help reduce driver stress and increase retention. In addition to helping with driver satisfaction, route optimization can help fleets meet customers’ expectations for delivery timelines while ensuring the highest number of deliveries with the least number of miles and drivers. Certain types of software also provide real-time routing that auto-corrects when factors like traffic or weather events impact efficiency.

Longer shifts often lead to driver fatigue, which leads to accidents and opens the door to expensive litigation and insurance premium increases. Fleet owners also have an opportunity to reimagine how they plan routes for drivers so that they are able to spend more time at home versus being committed to long shifts on the road. For example, instead of driving through smaller towns, consider having these locations be switch-off points from one driver to another.

Supply Chain Optimization

Transportation companies can also minimize supply chain risk by optimizing their supply chain management. Here are some things to consider when thinking about supply chain optimization:

- Use technology and data to your advantage: Using technology solutions in supply chain management can provide visibility into inefficiencies and supplier risk so that you’re able to remediate issues in a timely manner.

- Renegotiate with suppliers: To ensure that you’re getting the best rates possible, don’t be afraid to renegotiate. Cutting down on costs by renegotiating with suppliers can help you improve your profit margins.

- Communicate with suppliers: Communicate with key suppliers to gain visibility into their inventory, production, and purchase fulfillment status. In the event of shortages, it’s important to know how they’ll prioritize you in the context of their full customer list.

- Alternate supply sources: Gain as much visibility as possible into tier-two suppliers in case key suppliers can’t meet your demands. It’s important to be able to activate tertiary supplier relationships in times of crisis.

- Assess your supply chain risk: You’ll want to take a deep dive into your insurance to ensure that it can provide the financial relief your company needs should you experience supply chain issues. Consider looking into business interruption coverage and supply chain

disruption insurance.

Safety Training Programs

Continuously training employees about safety on the road helps prevent accidents. And if a driver does get into an accident, zero in on telematics data to deliver training that can help prevent something similar from reoccurring in the future. As newer drivers with less experience enter the transportation industry, regularly training them will be critical in helping reduce the likelihood of claims.

Cyber Security Controls

To maximize the benefits of technology solutions, fleet owners need to implement cybersecurity controls and best practices that minimize the probability of a successful data breach from happening. Regularly providing employees cyber security awareness trainings, implementing multi-factor authentication (MFA) for all users, and having an incident response plan are just a few of the steps you should take to improve your cyber security. If you do not have the internal resources to handle cyber security, consider partnering with a trusted vendor for their services. Additionally, many cyber carriers may not even consider selling you a policy if you do not have these cyber security measures in place.

Managing the Overall Cost of Risk & Insurance

Insurance premiums are higher and the overall cost of owning a fleet is greater, and as a fleet owner, you are left to figure out how to manage it all. With carriers increasing underwriting scrutiny as a response to unfavorable conditions, getting ahead of the underwriting submission process, preparing a narrative of your risk that carriers can easily understand, and investing wisely in both insurance and loss containment can be the difference between getting the coverage you need, or getting declined.

Though a hardened insurance market is undoubtedly difficult to navigate, current market conditions also highlight the importance of being as proactive as possible in managing the overall cost of risk to get the best underwriting results from carriers. Implementing these strategies pays dividends in good times, and especially in challenging times. Consider taking the following steps to help manage the overall cost of your risk and insurance:

- Identify your Risks and Understand how they Impact your Cash Flow: In order to know how to mitigate your risks and how you can best use insurance to financially protect your business, you need to identify the exposures your organization faces and the financial consequences should you fail to address them. Quantifying risk in dollar amounts empowers you to invest intelligently in loss controls and properly structure coverage to avoid coverage gaps and overlaps. This process also helps you see areas where you might be able to transfer risk to vendors or subcontractors.

- Regularly Conduct Risk Assessments: Because risks take all shapes and forms and come from many directions, regularly conducting risk assessments better positions your company to adapt to the constantly evolving risk landscape that characterizes the world today. When any of your operations or assets change, so do your risks. Communicate with your trusted advisor to ensure that insurance coverages align with these changes as they happen.

- Reconcile All Valuations: Insureds and brokers need to confirm all assets are measured accurately because most carriers are now requiring higher replacement cost values for the assets they insure due to inflation and rising replacement costs. Staying on top of the valuation process can also improve negotiation leverage in the market.

- Evaluate your Risk Tolerance: Understand how much coverage you’re purchasing and how deductibles impact your liabilities. If you have a higher risk tolerance, you may be able to lower premiums after reviewing for financial feasibility. Ask your advisor to evaluate creative program structures, like deductible buydowns, deductible indemnity agreements, captives, and parametric insurance (loss mitigation). Captives are an option that provide companies of all sizes more control over risk management and cost containment, which reduces the overall cost of risk.

- Invest in Loss Controls and Risk Mitigation Strategies: Investing in loss controls, such as telematics, driver training, and cyber security controls, has upfront costs, but these investments are usually insignificant compared to the financial burden of a loss. Underwriters want to see that both proactive and reactive measures are in place. Proactive loss controls are the actions you take to prevent claims from happening. This can take the form of using telematics for your auto fleet, or regularly educating your employees about safety on the job. Reactive loss controls are the corrective measures you take as a response to loss to prevent similar events from happening again in the future. For example, if you experience a cyber breach, what actions will you take to prevent a similar breach from happening in the future?

- Vet All Vendor Relationships: Understand how contracting with other parties can create risk for your business and then find ways to reduce this risk. Most companies rely on third-party service providers and vendors to support their business, and they introduce layers of risk into your organization. This can take the shape of cyber risk, supply chain risk, and more. When you are entering an agreement with vendors and service providers, all involved parties need to think about how contractual risk fits into the picture.

- Be Prepared for Your Renewal: Do not wait until the last minute: begin preparing for your renewal at least four months before coverage is bound. Develop and document a strategy to keep yourself and your advisor accountable throughout the renewal process so that you are able to do everything within your power to get the best terms from carriers. Work with your advisor to hold stewardship meetings to keep everyone informed of current market conditions and what to expect at renewal.

- Prepare a Narrative Underwriters will Understand: The underwriting data you provide to the market needs to be complete and easy to understand. In many cases, tailoring the data for input into various underwriting models will help expedite the process and result in better market feedback. Although it is not always the case, generally the price underwriters charge for uncertainty is greater than if they know the full scope of an account’s history and all underwriting information is provided in a user-friendly manner.

- Demand a Thorough Coverage Analysis from Carriers: Both you and your advisor should have full policy forms and endorsements on file. Doing an audit of all policies ensures coverages are adequate and meet your goals. In a hard market, insurance companies will look to include endorsements and policy language that limit or remove previous coverages. Be sure to address all policy changes.

A Trusted Advisor Partner to Traverse the Twists & Turns of Risk

Because of market conditions, it is also important for you to partner with an experienced advisor who understands the complexities of the transportation industry. Working with our team of experts can help you quantify your risks, determine where you are most financially susceptible to exposures, and determine which loss controls you should implement to protect your assets and investments.

Our transportation experts have seen countless scenarios play out and can provide resources to help you improve how you approach risk, and find insurance that meets your needs as they evolve. We know how to put you in a position where underwriters are more likely to see your risk profile in a favorable light.

We strive to become an extension of your team and deliver risk mitigation strategies and insurance architecture that align with your goals from day one. In addition to helping with the implementation of loss control strategies that help manage the overall cost of insurance, here are other ways we help clients in the transportation industry:

- Keeping you Abreast of Market Changes: We stay abreast of market changes so that you don’t have to and communicate how changes to underwriting standards impact your coverage.

- Access to Global Markets: Our team has access to global markets and knows how to align insurance coverage and risk mitigation coordination for global operations. We have strong, long-term relationships with the world’s top transportation insurance carriers.

- A Consultative Approach: In order to be as effective as possible, we shape our strategy around your business goals, needs, and values as they evolve. It’s our job to learn this information from you and adjust our approach to the insurance purchasing and risk mitigation process accordingly.

- Collaborating with Lenders: We help facilitate the conversation with lenders about how insurance fits into the transaction lifecycle for the projects in which you invest. Our experts provide guidance about risk mitigation at all stages of projects and help you communicate with lenders about how insurance protects investments and enhances profitability.

- Tailoring your Insurance Program: Determining the right coverages and limits for complex operations requires the highest level of expertise. With 35 team members averaging 20 years of industry experience, our team knows how to tailor insurance programs for clients’ unique needs.

- Loss Control Services: We provide insights and access to resources that reduce the likelihood of claims from occurring. Our goal is to establish a culture of risk management that prioritizes safety, compliance, and education, so that our clients can manage their exposures, stay ahead of the competition, and protect their most valuable assets.

- Providing Detailed Claims Analysis: Our in-house team of advocates helps expedite and manage the entire claims process so clients can maximize recovery and reduce their cost of risk. We identify what caused a claim to happen and provide recommendations about risk mitigation strategies to reduce the severity of claims in the future.

With underwriting scrutiny at an all-time high and insurers providing less favorable terms for coverage, now’s the time to work with a team of experts with a proven track record in the transportation industry.

Contact our transportation team today to learn more about how we can help you assess your risks and protect your assets and investments.

1 Josh Fisher, As recession concerns rise, driver shortage figures stall, FleetOwner, October 26, 2022

2 Josh Fisher, Ibid

3 What is third-party litigation funding and how does it affect insurance pricing and affordability?, Insurance Information Institute, July 27, 2022

4 Dale Porfilio, Social Inflation From Research to Actions, Insurance Information Institute, March 23, 2022

5 How Much Has Inflation Increased In 2022? And Are Prices Still Rising?, Forbes, December 12, 2022

6 Wayne Duggan, February CPI Report Shows Inflation Keeps Falling, Forbes, March 14, 2023

7 Inflation and the Auto Industry: When Will Car Prices Drop?, J.P. Morgan Chase, February 22, 2023

8 12-month percentage change, Consumer Price Index, selected categories, U.S. Bureau of Labor Statistics, Accessed March 20, 2023

9 Camila Domonoske, It’s not just buying a car — owning one is getting pricier, too, NPR, November 4, 2022

10 U.S. All Grades All Formulations Retail Gasoline Prices, U.S. Energy Information Administration, Accessed March 20, 2023

11 NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters (2023). DOI: 10.25921/stkw-7w73

12 NOAA, Ibid

13 Acronis Cyber Protection Operation Center Report, Acronis, Q3-Q4 2022

14 Commercial property/casualty market index, CIAB, Q4 2022

15 Insurance Economics Outlook, Insurance Information Institute, January 18, 2023

16 Stephanie Fox, The rise of nuclear verdicts and how to rein them in, Verisk, August 24, 2021

17 Corporate Verdicts Go Thermonuclear, Marathon Strategies, Accessed March 20, 2023

18 Loretta Worters and Jeremy Engdahl-Johnson, Inflation, Catastrophes, and Geopolitical Risks Weigh on 2022 P&C Industry Results, New Triple-I/Milliman Report Shows, Insurance Information Institute, February 7, 2023

19 Climate change and La Niña driving losses: the natural disaster figures for 2022, Munich RE, January 10, 2023

20 Insights into the 2023 Commercial Property Insurance Market | Property & Casualty, CBIZ, Accessed March 20, 2023

21 Commercial property/casualty market index, Ibid

22 Ryan Smith, US commercial insurance rates rise in Q4, Insurance Business Magazine, January 9, 2023

23 Commercial property/casualty market index, Ibid

24 Commercial property/casualty market index, Ibid

25 Steve Evans, Renewals: Catastrophe retro rates +50%, global property cat +37%, says Howden, Artemis, January 3, 2023

This document is intended for general information purposes only and should not be construed as advice or opinions on any specific facts or circumstances. The content of this document is made available on an “as is” basis, without warranty of any kind. Baldwin Risk Partners, LLC (“BRP”), its affiliates, and subsidiaries do not guarantee that this information is, or can be relied on for, compliance with any law or regulation, assurance against preventable losses, or freedom from legal liability. This publication is not intended to be legal, underwriting, or any other type of professional advice. BRP does not guarantee any particular outcome and makes no commitment to update any information herein or remove any items that are no longer accurate or complete. Furthermore, BRP does not assume any liability to any person or organization for loss or damage caused by or resulting from any reliance placed on that content. Persons requiring advice should always consult an independent adviser.

Baldwin Risk Partners, LLC offers insurance services through one or more of its insurance licensed entities. Each of the entities may be known by one or more of the logos displayed; all insurance commerce is only conducted through BRP insurance licensed entities. This material is not an offer to sell insurance.

Comments are closed.